Check out this information on federal and private loans. Use these resources to make smart decisions.

Federal Loans

Subsidized vs. Unsubsidized Student Stafford Loans

There are two types of Federal Stafford Loans: subsidized and unsubsidized. Depending on household income, a student can be eligible for one or both. In the financial aid award letter, the college specifies for which loans the student is eligible. If you aren't able to completely fund your college education with scholarships, Stafford loans are the first loan option you should consider due to their rate and repayment policy.

Parent Direct PLUS Loan

Parents of dependent undergraduate students can borrow a PLUS loan to help pay for their child’s education. The PLUS loan has a fixed interest rate and allows parents to borrow up to the remaining cost of attendance (cost of attendance minus any financial aid) determined by the school. Financial need is not required in order to be eligible to borrow a PLUS loan. A borrower must not have an adverse credit history and part of the application process includes a credit check. If a parent borrower has an adverse credit history, the parent can still borrow a PLUS loan if they have an endorser (co-signer) or the student could qualify to borrow the higher loan amounts available to Independent students through the Unsubsidized Direct Loan Program due to the denial of a PLUS loan to the parent.

There are two types of Federal Stafford Loans: subsidized and unsubsidized. Depending on household income, a student can be eligible for one or both. In the financial aid award letter, the college specifies for which loans the student is eligible. If you aren't able to completely fund your college education with scholarships, Stafford loans are the first loan option you should consider due to their rate and repayment policy.

- Subsidized Stafford Loans are need-based loans. The government pays the interest while the student is in school, if applicable, and during the grace period before repayment begins.

- Unsubsidized Stafford Loans are not based on income and not all students are eligible for the maximum loan amount. Eligibility is determined by the student’s year in school, other financial aid awards, and the estimated cost of attendance. Students who borrow unsubsidized Stafford Loans are responsible for all interest that accumulates while they are in school, in deferment, and during the grace period.

- $5,500 for first-year students enrolled in a program of study that is at least one full academic year. Only $3,500 of that can be subsidized loans.

- $6,500 if you've completed your first year of study and the remainder of your program is at least one full academic year. Only $4,500 of that can be subsidized loans.

- $7,500 if you've completed at least two years of study and the remainder of your program is at least one full academic year. Only $5,500 of that can be subsidized loans.

Parent Direct PLUS Loan

Parents of dependent undergraduate students can borrow a PLUS loan to help pay for their child’s education. The PLUS loan has a fixed interest rate and allows parents to borrow up to the remaining cost of attendance (cost of attendance minus any financial aid) determined by the school. Financial need is not required in order to be eligible to borrow a PLUS loan. A borrower must not have an adverse credit history and part of the application process includes a credit check. If a parent borrower has an adverse credit history, the parent can still borrow a PLUS loan if they have an endorser (co-signer) or the student could qualify to borrow the higher loan amounts available to Independent students through the Unsubsidized Direct Loan Program due to the denial of a PLUS loan to the parent.

- For more information and to apply go to: https://studentaid.ed.gov/sa/types/loans/plus

You must “Accept” or “Deny” these loans on your college/university account. If you accept the loans, you must then complete loan entrance counseling at studentloans.gov

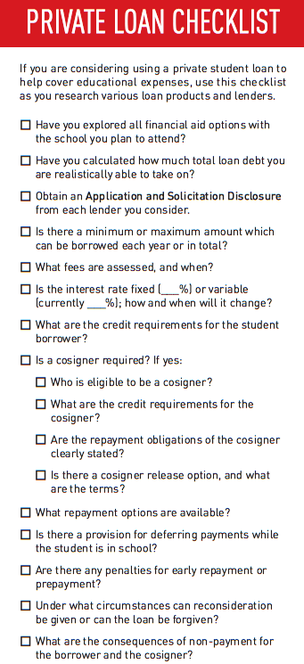

Private Loans

Private student loans are consumer loans made to individuals to help pay for college expenses. They are provided by both for-profit and non-profit lending institutions. They are not backed by the federal government, but they are regulated by consumer credit laws.

Minimize private loans when possible because interest rates are higher (6.17% - 11.26%) and repayment plans are less flexible. An unsubsidized loan (available regardless of financial need) is still a better option than a private loan. Beware of educational loan offers that seem “too good to be true”. Though you may get the funds easily, you may pay more through high interests rates. Places to get private loans...

Use this website to find out common private loaners based on your college of attendance.

Private Loan Comparison websites:

Use this loan calculator to see what your monthly payments will look like after college.

Loan Tips:

Minimize private loans when possible because interest rates are higher (6.17% - 11.26%) and repayment plans are less flexible. An unsubsidized loan (available regardless of financial need) is still a better option than a private loan. Beware of educational loan offers that seem “too good to be true”. Though you may get the funds easily, you may pay more through high interests rates. Places to get private loans...

- Your bank/credit union or your cosigner’s bank/credit union

- Wells Fargo, Members First, PNC, Union Community Bank, etc.

- Consumer Banks such as Sallie Mae

Use this website to find out common private loaners based on your college of attendance.

- ELM Select: www.elmselect.com/#/

Private Loan Comparison websites:

- Credible: https://www.credible.com/student-loans

- Simple Tuition: https://www.simpletuition.com/

- Lendedu: https://lendedu.com/

Use this loan calculator to see what your monthly payments will look like after college.

- Loan Calculator: http://www.finaid.org/calculators/loanpayments.phtml

Loan Tips:

- My Smart Borrowing : http://www.mysmartborrowing.org/#intro

- You Can Deal With It: http://www.youcandealwithit.com/

- College Board: bigfuture.collegeboard.org/pay-for-college/loans?SFMC_cid=EM19163-&rid=30063530

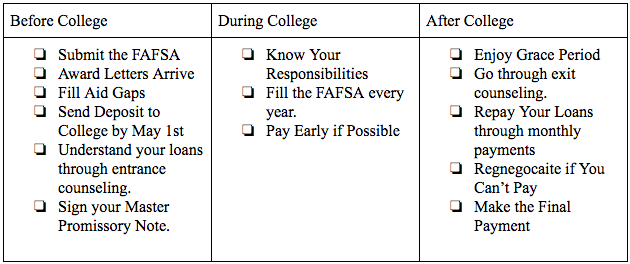

Loan Timeline

|

|

Loan Consequeces

If payments for your federal loans become 270 days delinquent, your lender/loan servicer will take steps to place the loan in default. Don't let this happen! If you have difficulty making your loan payments, contact your servicer immediately. Defaulting on your student loans will have consequences, such as…

- Damage to your credit rating - This affects your ability to get future loans, such as an auto loan or mortgage, obtain housing and even employment.

- Garnishment of your wages - Yes, the lender/servicer has the right to take money directly from your paycheck to help repay your federal loans and they don't need your permission to do so.

- Withholding of your tax refunds - Looking forward to a big payday at tax time? Not if your loans are in default. Your tax refund can be directed to your lender/servicer to help pay your federal loans.

- Loss of eligibility for federal and state financial aid - If you ever want to go back to school and receive financial aid to help with the costs, you might not qualify if your loan is in default.

Options IF You Can't Pay On Time

Can’t Pay? If you're struggling to make your monthly payments, don't despair. Solutions are available.

- Change Your Due Date - Make sure you have money in the bank when it's time to pay your bill.

- Reduce Your Monthly Payments -The repayment plan you choose affects the amount you pay each month.

- Postpone Payments - Find out if you qualify for a deferment or forbearance, which allows you to postpone monthly payments.

- Loan Consolidation - Combine one or more existing student loans into a single new loan.

- Loan Discharge and Loan Forgiveness - If you meet the eligibility criteria for loan discharge or forgiveness, your loan balance will be paid for you.